You're Never Really Done: Why Recurring Capex Scales Faster Than Your Real Estate Portfolio

You're Never Really Done, Really

There's a fantasy that shows up early in every investor's head: at some number of doors, the portfolio runs itself. The mortgage gets paid down, the rent checks show up, and you get to be the person who owns real estate instead of the person who works on real estate.

Then the sewer line backs up.

Not metaphorically, actually. A four-inch cast iron pipe under a slab that was fine for forty years decides it's done being fine, and now you're getting quotes for trenchless repair on a Tuesday afternoon instead of doing literally anything else you had planned.

The math nobody puts in the pro forma

Every unit you own is a small machine with parts that wear out on their own schedule, and the schedules don't care about your spreadsheet. Roofs go around year 20-25. Water heaters, 10-15. HVAC systems, 12-20. Sewer laterals, whenever the tree roots finish their work, which is not a schedule at all.

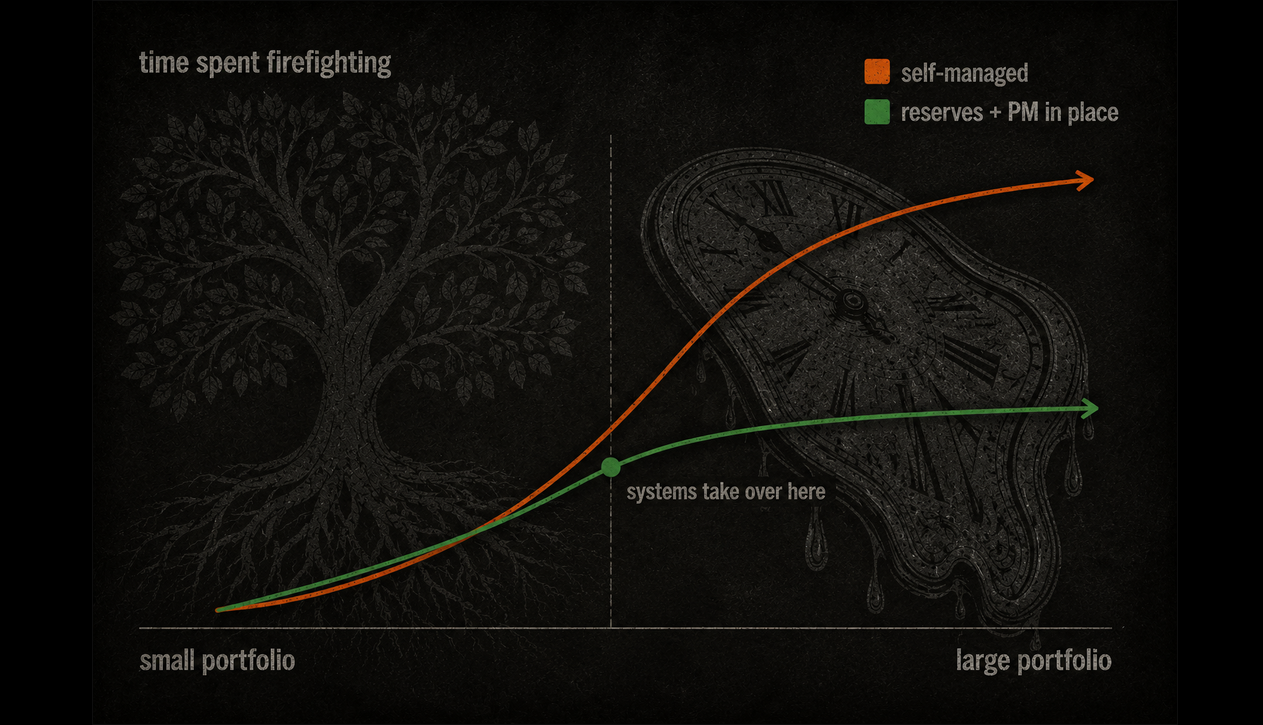

Here's the part that catches people: this isn't linear, it's closer to a rolling average that never resolves. One unit, you might go three years without a real capex event. Ten units, you're averaging one every few months. Fifty units, you have effectively become a person with a part-time job called "waiting for the next call."

The portfolio didn't get less work per door as it scaled. It got more total work, and the total work is what determines whether you're free or not.

Cash flow and time are different currencies

A lot of investors track the first one obsessively and ignore the second one completely. Net cash flow per door looks great on paper right up until you tally the hours: the calls with the plumber, the three contractor quotes because the first one felt like a number pulled from the sky, the trip to Home Depot because the property manager "can handle everything" except apparently not this.

Positive cash flow that requires your ongoing attention isn't passive income. It's a job with irregular hours and no sick days, and the size of that job scales with the size of the portfolio, often faster, because older buildings compound their maintenance needs the same way compound interest works, just in the wrong direction for you.

The actual finish line

Getting to "done" isn't a unit count. It's the point where the property's maintenance needs stop being your problem to solve in real time. That happens through a few specific mechanisms, not through wishing:

Reserves sized to reality, not to hope. Most underwriting uses a capex reserve that's a rounding error compared to what a roof or a HVAC replacement actually costs. If the reserve is real, funded, untouched, sized off actual replacement costs for your specific assets, then a failure is a withdrawal, not an emergency.

A property manager who owns the vendor relationship, not just the rent collection. The difference between a PM who forwards you every maintenance ticket for approval and one who has standing authority and a trusted contractor bench is the difference between still having a job and actually not having one.

Systems, not favors. If your handyman cousin is your maintenance plan, you don't have a maintenance plan, you have a single point of failure with a phone number. Real systems survive turnover: your handyman cousin retiring shouldn't change your monthly workload.

Enough scale to average out, or little enough to not need to. This sounds contradictory, but it isn't. A big enough portfolio with the right structure turns "surprise repairs" into a predictable annual line item, smoothed by volume. A small enough portfolio, fully outsourced, just costs you a management fee instead of your Saturday. The failure mode is the middle ground, too big to ignore, too small to have real systems, and you're doing it all yourself.

The honest version of retirement

Retiring from real estate doesn't mean the properties stop needing anything. Buildings always need something; that's what buildings are. Retiring means the need no longer routes to you. The call goes to a property manager who has both authority and a reserve account. The invoice gets paid without your signature. You find out about the sewer line in a monthly report, not in a moment of dread.

Until that's true, you don't own a passive portfolio, you own a second job that happens to appreciate. Which might still be worth it. Just don't confuse it with being done.