The 1031 Exchange nobody tells you needs a hard hat.

Quick disclaimer before we go anywhere: I am not a CPA, not an accountant, not a tax attorney, and I have exactly zero business telling you what to do with your capital gains. Nothing below is tax advice. If a 1031 exchange is on your radar, go talk to a qualified intermediary and a CPA who actually knows your numbers. This isn't that conversation.

What I do know is what happens once the tax strategy meets a job site. That's where things get interesting.

The 1031 Exchange nobody tells you needs a hard hat-

Every 1031 article on the internet reads like it was cloned from the same template. Sell, defer, roll the proceeds, don't touch the cash, 45 days to identify, 180 days to close. Fine. Accurate. Boring. I'm not adding to that pile.

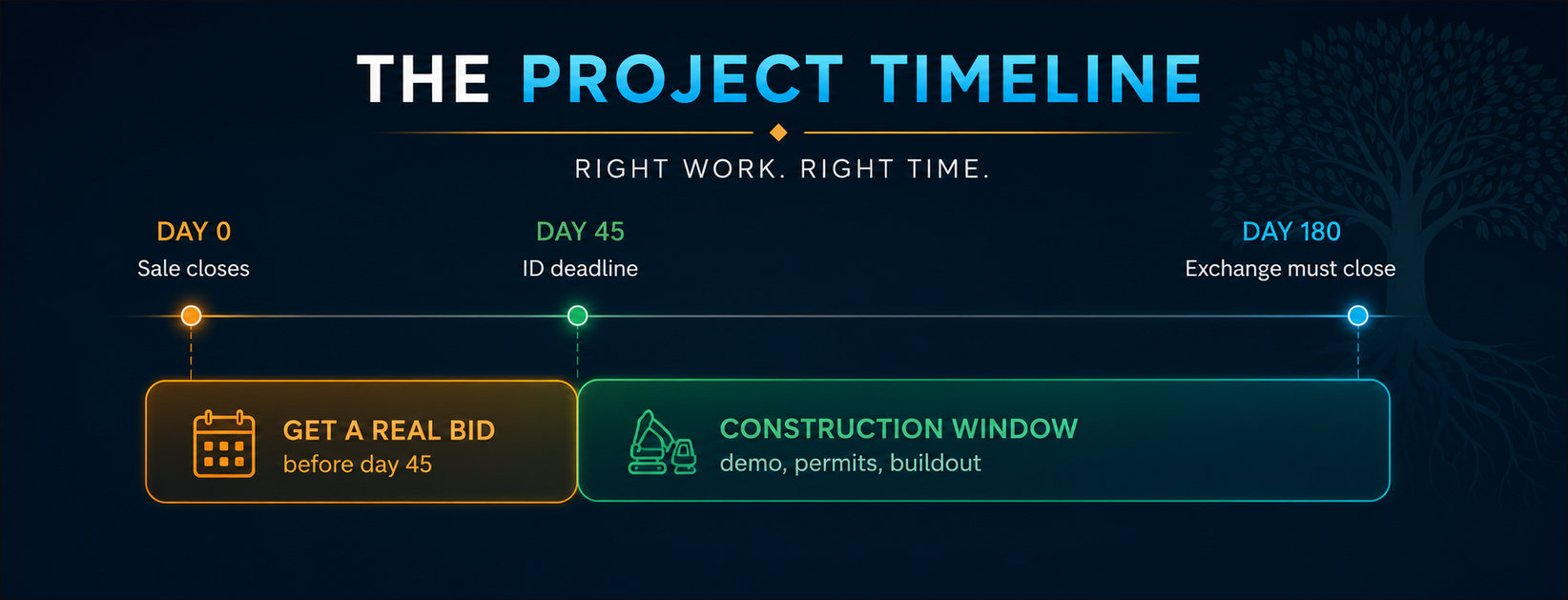

Here's the version nobody writes about: what happens when the replacement property isn't move-in ready. Maybe it needs a facelift. Maybe it needs its soul rebuilt from the studs out. That's a construction exchange, and it's the spot where I've watched perfectly good tax strategy get mugged by a bad renovation timeline.

The IRS Clock Doesn't Negotiate With Your Contractor

In a construction exchange, your money never touches your hands. It sits with an intermediary, who uses it to fund improvements on the new property before you ever take title. All of it, demo, permits, buildout, has to wrap inside the same 180-day window as the exchange itself.

180 days sounds generous. It is not. I've watched simple commercial rehabs blow past that deadline just waiting on a permit reviewer to open an email, before you even factor in a change order or a transformer on backorder.

Miss the deadline, and whatever's unfinished doesn't get a grace period. It gets treated as boot. Taxable. You did all that paperwork to defer a tax bill, and a slow subcontractor just handed a chunk of it right back to the IRS.

The Mistake Happens Way Before Demo Day

It's rarely the tax structuring that goes sideways. It's earlier, during the 45-day identification sprint, when someone's under pressure to lock in a property and nobody with actual construction eyes has walked it yet.

A building pencils out on paper. Looks fine from the parking lot. Nobody's popped a panel cover or gotten a bid from someone who has to answer to a deadline instead of just a number. The identification gets locked in on a guess, and by the time real pricing rolls in, the schedule's already tight and now the budget's wrong too.

By the time I get the call, the choices are both bad: push forward on a scope that's underfunded and gamble on the deadline, or eat a change order after the exchange is already locked in stone.

Before You Lock In That Replacement Property

So if you're sitting on a 1031 right now with a property that needs work, how confident are you, really, that the scope you've got matches what's actually behind those walls?

And if that number's off by even 15%, what does that do to your 180-day window?

Most investors don't find out the answer until they're already three weeks into demo and a permit reviewer just went quiet. If you'd rather find out before you identify the property than after, that's a fifteen-minute conversation, not a sales pitch. Book the call and bring me the address, I'll tell you what I'd actually worry about.